Doug Hutchinson

Doug Hutchinson

{kind=link}

The Benefits of Investing Early for Retirement

When I was a kid, it annoyed me when relatives I only saw during the holidays would exclaim, “Look at how much you’ve grown!” Now that I’m an adult,...

When we talk with clients about saving and investing for the future, the conversation usually steers toward retirement planning – IRAs, 401(k)s, pensions, Roth IRAs and so on. After all, retirement is when all of your hard work, careful saving and well-intentioned investing pays off. It’s when you’re finally supposed to be able to live the good life.

But investing isn’t always about retirement planning. Nor should it be. While many people share the same goal of retiring with financial security, there are other life goals that require careful saving and planning.

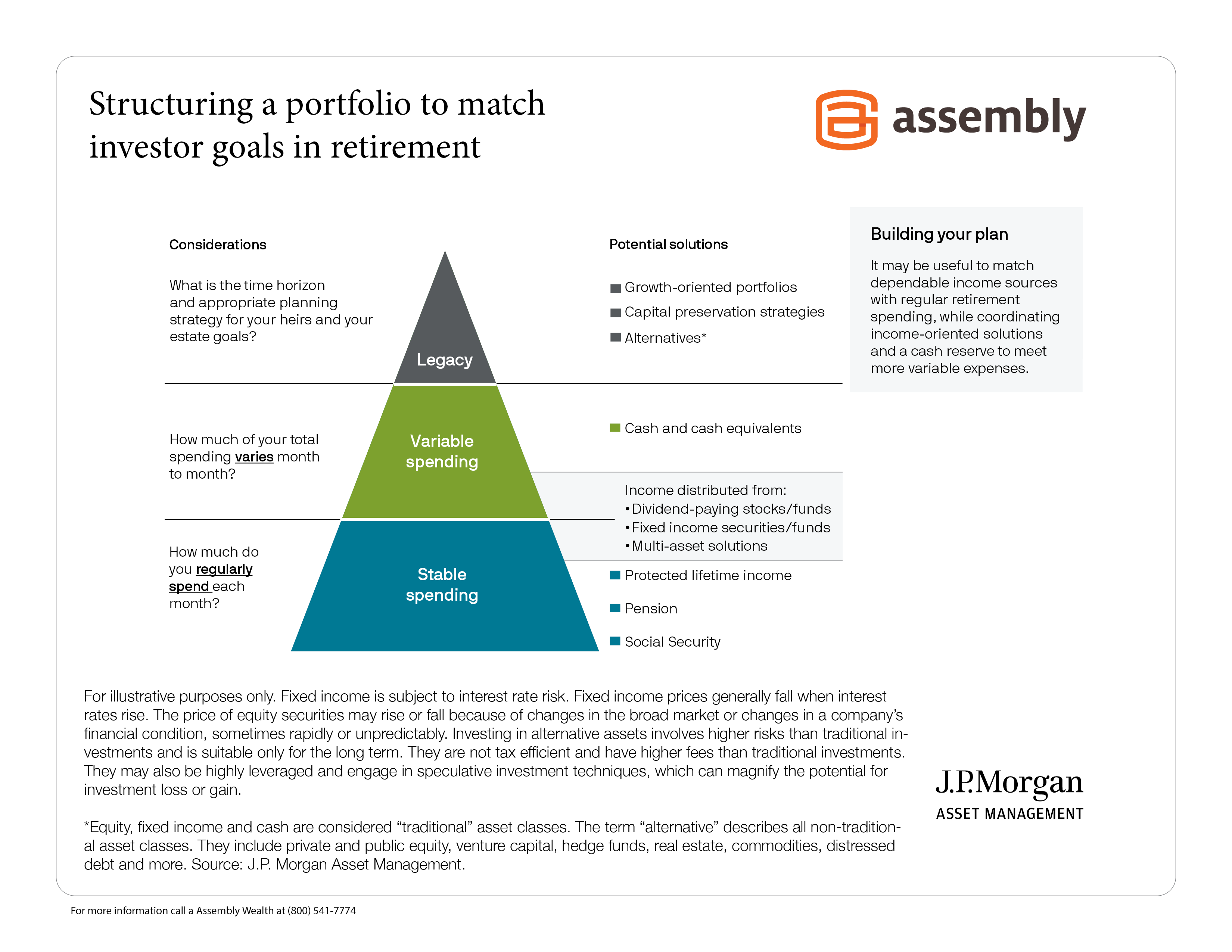

Your financial plan should include needs, wants and anything you may want to leave as a legacy. As the chart below illustrates, each of these categories require different investment strategies.

Click to see larger image

Retirement planning infographic comparing investment strategies for wants, needs and legacy

Food, housing and anything you can’t live without fall into the “need” category. The investments you choose to cover the cost of those needs should be stable, fixed sources of income such as a pension, fixed annuities and Social Security payments.

What does an ideal retirement look like for you? Do you want to upgrade your home or buy a second home? Do you have plans to travel? Would you sleep easier knowing you’re prepared for a “just in case” scenario such as elderly parents needing care? These are all example “wants.”

Once your retirement needs and wants are fulfilled, you may want to allocate assets to loved ones or a charitable organization. There are different strategies and investment tools you can use depending on how you choose to share your wealth.

Have questions now? Go here to contact us now.

As we mentioned at the outset of this article, investors tend to be hyper-focused on retirement planning. But once you analyze your needs, wants and legacy goals, most investors find a one-size-fits-all retirement plan doesn’t serve them well.

The four examples below represent a few of many possible life goals an investor may have. As you read through the examples below, think about your non-retirement goals and how they fit (or don’t fit) into your current investment plan.

Buying a New Home – Saving money in a brokerage account and investing it according to your available time horizon is one approach to achieving this goal. But someone who plans to buy a house in 20 years may have more leeway to invest in riskier assets compared to someone who wants to buy a house in less than 10 years. The investor with a shorter time horizon may benefit from reduced equity exposure and a more balanced strategy.

Saving for Grandchildren’s College Education – For most investors, saving for a grandchild’s college education means having a fairly lengthy time horizon. A diversified equity approach in a tax-advantaged vehicle such as a 529 plan may be a good option.

A Trip Around the World – The cost of a once-in-a-lifetime trip would probably be less than the cost of a second home or college education. For this goal, a fixed-income or low-risk approach to earn some interest may be a good option.

Charitable Donations – Donating to charity can reduce taxable income and provide much-needed support to nonprofit organizations. A donor-advised fund or charitable remainder trust funded with securities are two ways to leave a meaningful legacy. Establishing a fund during peak earning years can also lay the foundation for a purpose-driven retirement where you may have abundant time but limited funds.

When planning for the future, there are a lot of variables to consider. At Assembly Wealth, we’ve helped hundreds of individuals and families create a comprehensive financial plan. For help defining your goals or choosing a savings and investment strategy, contact us here to reach out and schedule a free consultation.

When I was a kid, it annoyed me when relatives I only saw during the holidays would exclaim, “Look at how much you’ve grown!” Now that I’m an adult,...

There are some long-standing retirement “rules of thumb” that still show up in conversations all the time: Withdraw 4% a year, and you’ll never run...

While some investors strive to beat the market, others use personal goals to measure their success. Goals such as: Paying for a child’s education ...