Doug Hutchinson

Doug Hutchinson

How to Avoid Dollar-Cost Ravaging Your Retirement Savings

It may look like a typo, but dollar-cost ravaging is a real thing — and a serious problem for some retirees. As you may have guessed, the name is a...

Many people assume, once they retire, the hard part is over. Money has been saved, investments have grown, and now it’s time to enjoy the rewards. But the reality is, choosing how much to withdraw and when can be challenging, especially when your portfolio value has decreased due to a market downturn.

Relying on rigid withdrawal rules can actually shorten the lifespan of your savings. A dynamic spending and withdrawal plan can help you strike a balance between enjoying retirement and help shield your nest egg from market volatility.

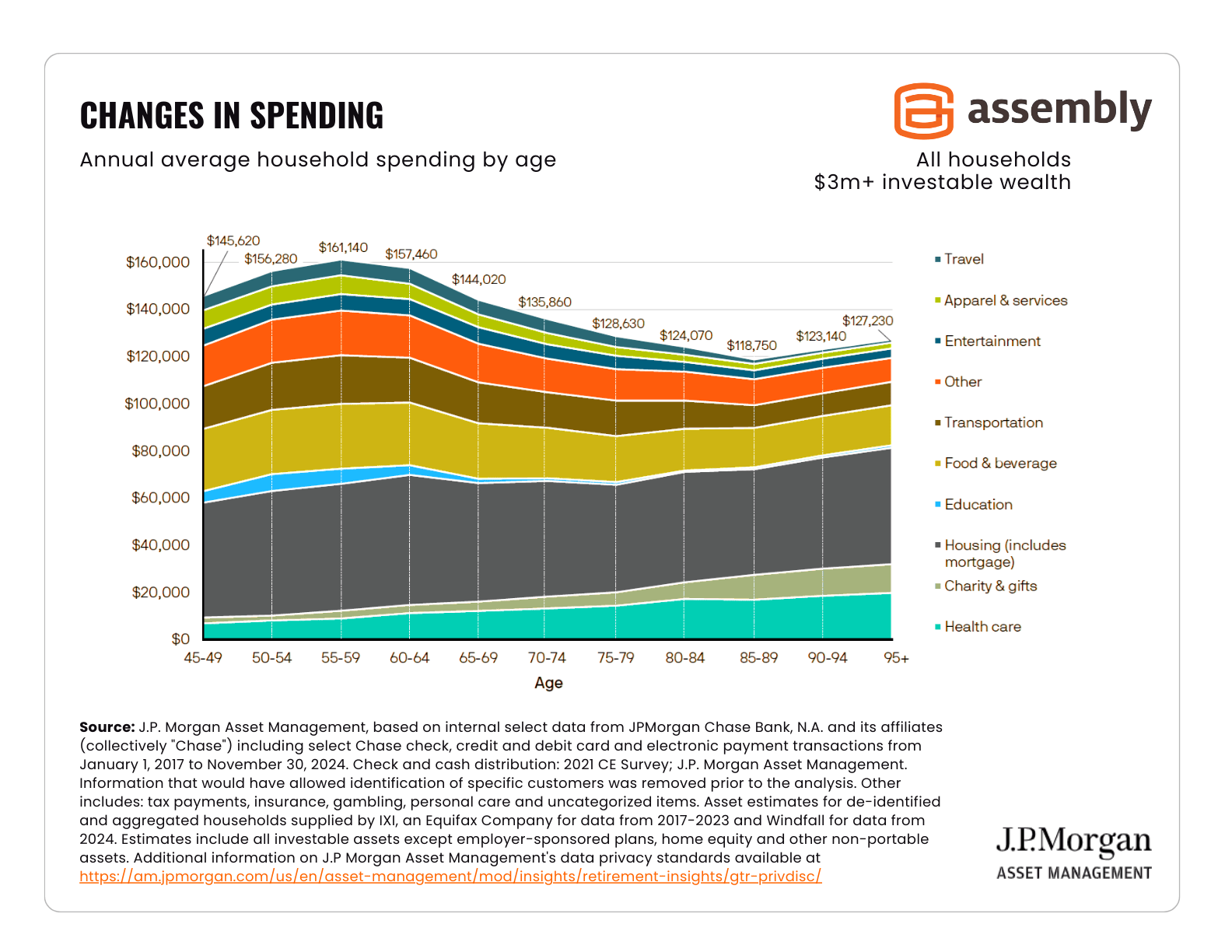

As the chart below shows, expenses tend to peak during midlife and reach their lowest point in early retirement. After age 80, spending may increase due to medical costs.

Click the image to view it in full size

SOURCE: JP Morgan Guide to Retirement 2025

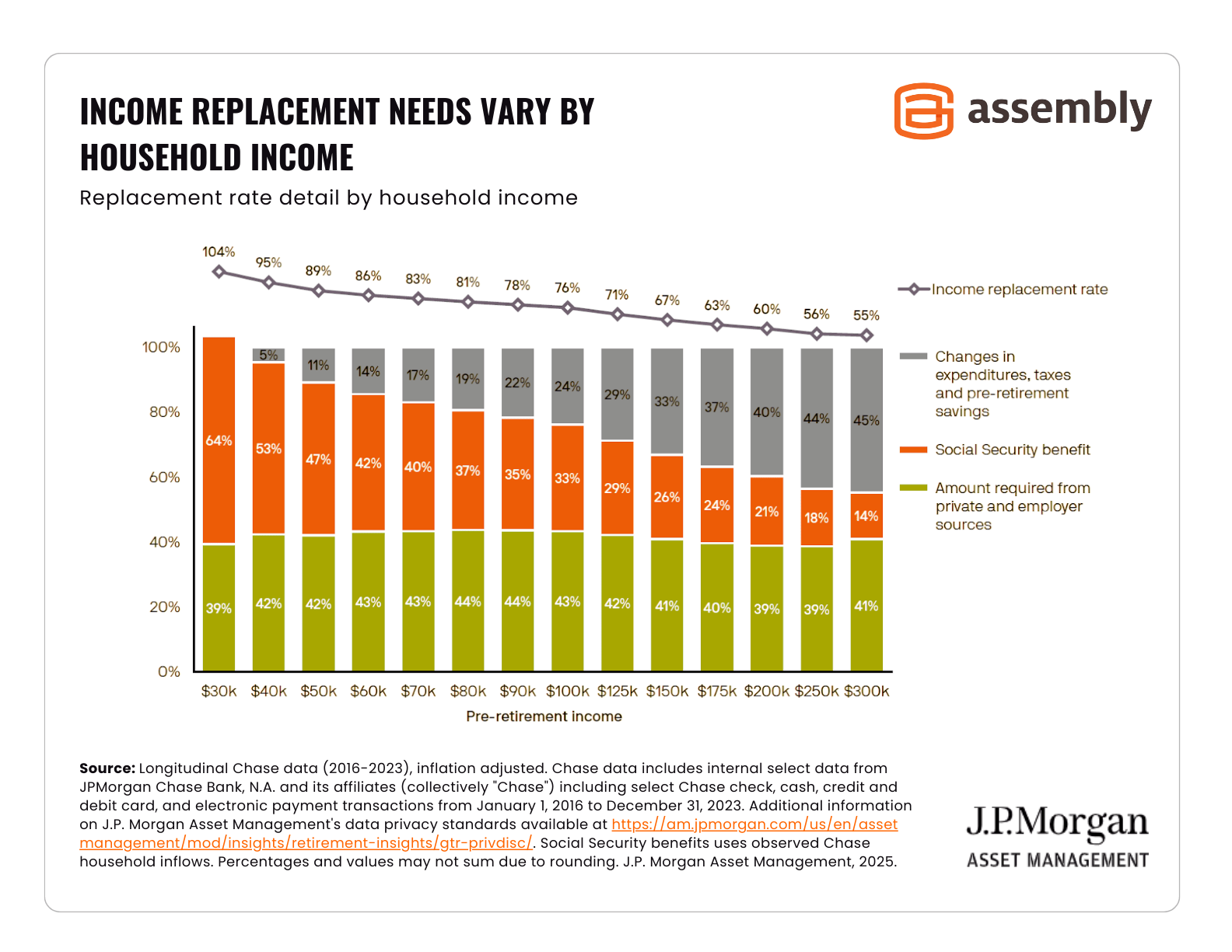

Everyone’s situation is different, but high-income earners generally need less money in retirement to maintain the same lifestyle. About one-third less.

But there’s something many retirees don’t account for…

Click the image to view it in full size

SOURCE: JP Morgan Guide to Retirement 2025

A significant number of retirees (60%) experience spending volatility during their first three years following retirement. After that, spending levels out until it becomes irregular again between the ages of 75-80 for more than half (52%) of retirees (source: JP Morgan Guide to Retirement 2025, slide 28).

A financial planner can help you create a dynamic spending plan that will allow you to prepare for unexpected expenses and minimize the impact of market volatility on your savings.

Our clients receive a unique plan tailored to their needs and goals. But here’s an example to illustrate the idea:

Retiree Reese has $3 million in retirement savings and needs $80,000 per year to cover basic expenses. Reese loves travel and wants to do some remodeling, but doesn’t want to dollar-cost ravage their retirement savings.

Reese’s financial advisor suggests the following:

If the market takes a dip, Reese will withdraw no more than $90,000 ($80,000 for expenses plus a buffer for inflation). When Reese’s investments perform well, Reese’s travel and home improvement funds get a boost. This dynamic spending and withdrawal strategy ensures Reese’s basic needs are met and Reese has “breathing room” for spending fluctuations.

One of our clients is extremely frugal despite having a very high net worth. His advisor had to nudge him to spend some of his money and enjoy life. The client is currently on a long vacation, enjoying his wealth of life!

His experience is not unusual. After many years of saving, many people don’t want to see their account balances decrease. They may even seek permission from their advisor to withdraw additional funds beyond what is needed for basic necessities.

After working hard all your life, you should be able to enjoy retirement! A wealth manager can help calculate how much (or how little) you can withdraw each year based upon anticipated needs, market fluctuations and your retirement goals.

Account Consolidation: Many clients come to us with multiple 401(k)s and brokerage accounts. We help them consolidate everything into one account, which makes planning and budgeting much easier.

Annuities: We’ve also helped several clients move annuity investments to lower-cost annuity options. This helps ensure the annuities meet the client's cash flow needs in retirement.

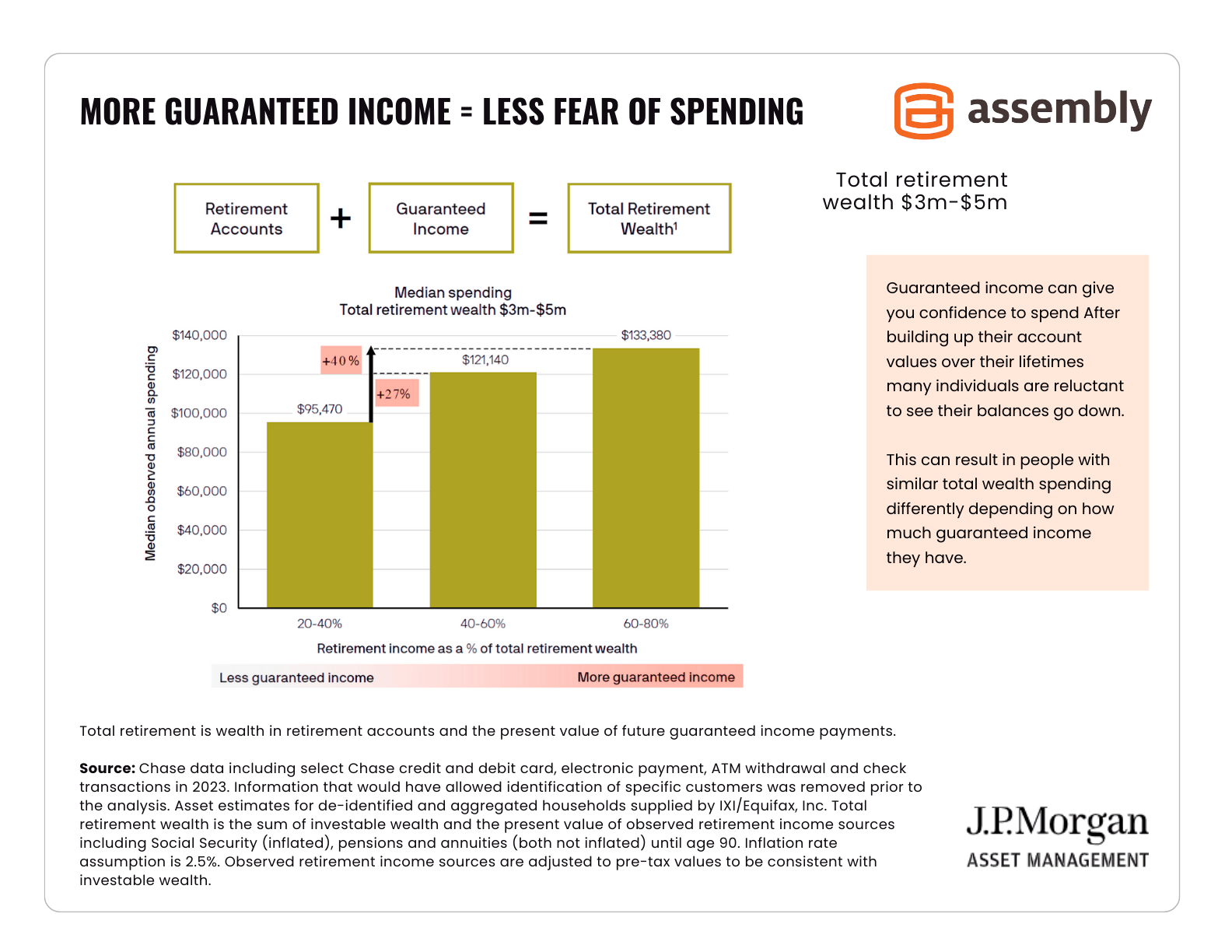

Still working? A wealth manager can help you find ways to increase guaranteed income so you feel more secure about making withdrawals.

As the chart below shows, retirees who get 60–80% of their income from guaranteed sources have the confidence to spend up to 40% more. A few examples of guaranteed income include: social security, annuities and defined benefit plans.

Click the image to view it in full size

SOURCE: JP Morgan Guide to Retirement 2025

Our friendly and experienced wealth management team can create a dynamic spending and withdrawal strategy that allows you to fund your retirement goals. Contact us online or by phone (415) 541-7774.

Related Reading:

Disclaimer: Assembly Wealth (“Assembly”) is an SEC-registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only.

All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios. Information presented represents an opinion as of the date published and should not be considered an investment recommendation.

Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

It may look like a typo, but dollar-cost ravaging is a real thing — and a serious problem for some retirees. As you may have guessed, the name is a...

Saving for retirement can feel like an uphill battle, even for couples. Planning for retirement solo can feel both liberating and daunting. You get...

While some investors strive to beat the market, others use personal goals to measure their success. Goals such as: Paying for a child’s education ...