Doug Hutchinson

Doug Hutchinson

Understanding Trump Accounts

Trump Accounts are a new type of investment vehicle to help young Americans save for the future. They have rules that are similar to an Individual...

Index replication is an investment strategy that involves buying a basket of stocks to replicate an index, such as the S&P 500. The strategy got a major boost in the 1990s with the launch of SPY, an ETF (Exchange-Traded Fund) that allows individual investors to buy every stock in the S&P 500 index with a single trade.

Today, there are hundreds of mutual funds and Exchange-Traded Funds (ETFs) that seek to replicate the performance of the S&P 500, Russell 1000 and many other indices. There are, however, some drawbacks to owning ETFs and mutual funds that mirror an index versus owning the individual stocks.

Direct indexing is the opposite of an ETF. Instead of buying a single fund, Direct Indexing involves buying many (sometimes all) of the individual stocks that make up an index, such as the S&P 500.

With direct indexing, an investor gains exposure to both the winners and losers in an index. This allows for tax-loss harvesting in a taxable investment account.

Tax loss harvesting involves selling a stock or other security for less than what you paid for it and using the losses to offset income from any securities sold for a profit. An investor can use net losses to reduce their taxable income up to $3,000 per year. Any amount above and beyond the $3,000 annual limit can be carried forward to future years. Learn more about tax loss harvesting rules.

Here’s an example scenario to illustrate the point above:

Your financial advisor has done some preliminary tax calculations, and the stocks you sold for a profit earlier this year have pushed you into a higher tax bracket, but just barely. The advisor recommends selling some investments at a loss to cancel out some of the profits — so you can possibly return to a lower tax bracket.

How does this apply to direct indexing? If you own the individual stocks within the S&P (versus a single ETF or mutual fund), you have the option to sell any holdings that may have declined in value to offset profits.

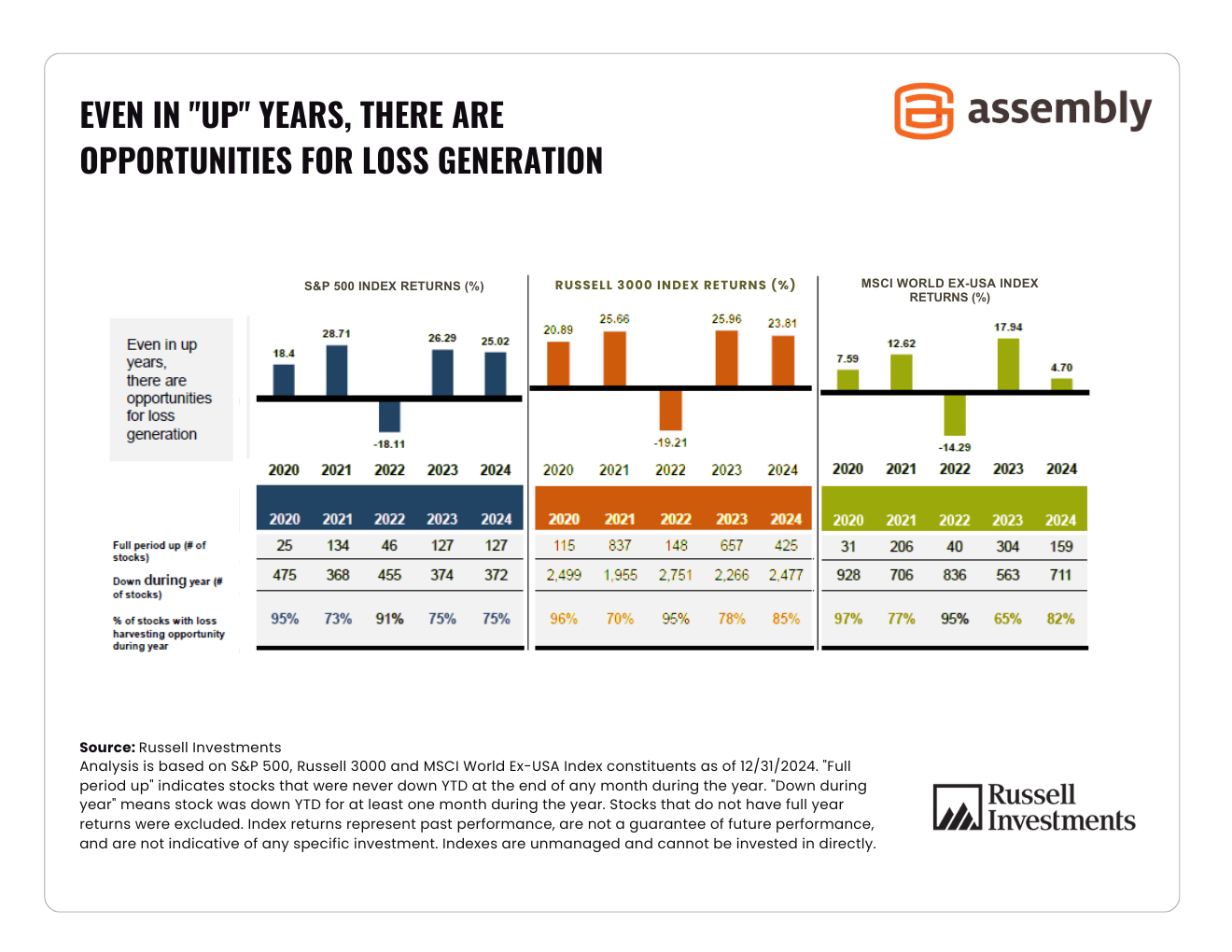

As the chart below shows, even when the S&P 500 is positive for the year, there are still plenty of opportunities to harvest losses on individual positions. But this is only possible if the investor owns individual stocks instead of the full index in a single fund.

Click the image to view it in full size

SOURCE: Russell Investments

Everyone who purchases an index fund gets the exact same basket of stocks. Investors who want to avoid owning certain companies can’t customize their portfolio. For example:

In either scenario, Direct Indexing would allow the investor to customize their portfolio.

Direct Index investing is often done through a Separately Managed Account (SMA). This taxable account is typically managed by the investor’s financial advisor or a Direct Indexing manager hired by the financial advisor.

Separately Managed Accounts can:

An experienced financial advisor can help you transition an existing portfolio of stocks into a Direct Indexing portfolio. The process goes something like this:

|

Goal |

Index Mutual Funds |

ETFs |

Direct Indexing |

|

Seeks to track performance of a market index |

Yes |

Yes, typically |

Yes, typically |

|

Ability to loss harvest individual positions in the index |

No |

No |

Yes |

|

Ability for investor to customize portfolio |

No |

No |

Yes |

|

Ability to transition existing portfolio of stocks |

No |

No |

Yes |

There are a few drawbacks to Direct Indexing versus buying an index fund:

Initial Cost — A single index fund can typically be purchased for a few hundred dollars or less. The minimum investment to get started with Direct Indexing is typically $100,000.

Tracking Error — A Direct Indexing strategy will rarely be able to track an index perfectly. For example, the Direct Indexing manager may not own all the positions in the index but will select securities with characteristics similar to those of the broad benchmark (yield, sector exposure, etc.) But, because of these differences, an investor should be prepared for some performance variation compared to the benchmark.

Tax-Loss Harvesting Opportunities Diminish Over Time – In a rising market, the opportunity to harvest additional losses from year to year will decline over time as stock values rise.

Greater Number of Trades – The financial advisor or Direct Indexing manager will harvest losses in the portfolio throughout the year to offset gains and avoid creating a tax liability. An investor with a Direct Indexing strategy should expect to see more trades than in a typical portfolio.

The main benefit of a Direct Indexing portfolio is the opportunity for greater tax efficiency. So it typically makes sense to utilize a Direct Indexing strategy in a taxable account versus a tax-deferred account (such as an IRA). That said, another benefit of Direct Indexing is the ability for customization, which can be done in both tax-deferred accounts and taxable accounts.

A Direct Indexing strategy can be very time-consuming and complex for a Do-It-Yourself investor. An individual investor will have to constantly monitor the portfolio for any potential tax lots that can be sold at a loss. The investor will also have to navigate potential wash sales with every buy and sell decision. Fortunately, a financial advisor or Direct Indexing manager will have software that does all of this manual work automatically.

An individual investor can save a lot of time and trouble by relying on a trusted financial advisor to implement and manage a Direct Indexing strategy. To learn more, feel free to reach out to an advisor at Assembly Wealth who will help you decide if a Direct Indexing account is a good fit for you and your financial goals. Contact us online or give us a call at (415) 541-7774.

Disclosure:

The S&P 500 Index measures the performance of 500 large U.S. companies, the Russell 3000 Index measures the performance of the broad U.S. equity market and the MSCI World ex USA Index measures equity market performance in developed markets outside the United States. Indexes are unmanaged and cannot be invested in directly.

Disclaimer:

Assembly Wealth (“Assembly”) is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Information presented represents an opinion as of the date published and should not be considered an investment recommendation. Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

Trump Accounts are a new type of investment vehicle to help young Americans save for the future. They have rules that are similar to an Individual...

As we age, we accumulate things: workout equipment, kitchen gadgets and 401(k) accounts from different jobs. The workout equipment and gadgets may be...

The 2025 Budget Reconciliation Bill was packed with tax law changes. Some are already in effect, others activate on January 1st, 2026.To ensure you...