Doug Hutchinson

Doug Hutchinson

Understanding Trump Accounts

Trump Accounts are a new type of investment vehicle to help young Americans save for the future. They have rules that are similar to an Individual...

Selling a home can be exciting, especially when you receive a six, or even seven-figure payout. Many people aren’t sure what to do with such a large amount of money.

There isn’t a one-size-fits-all answer, but we’ll share some suggestions in the article below. The best option will depend on your circumstances. We’ll also share recent stats about how much profit people make (on average) from selling a home.

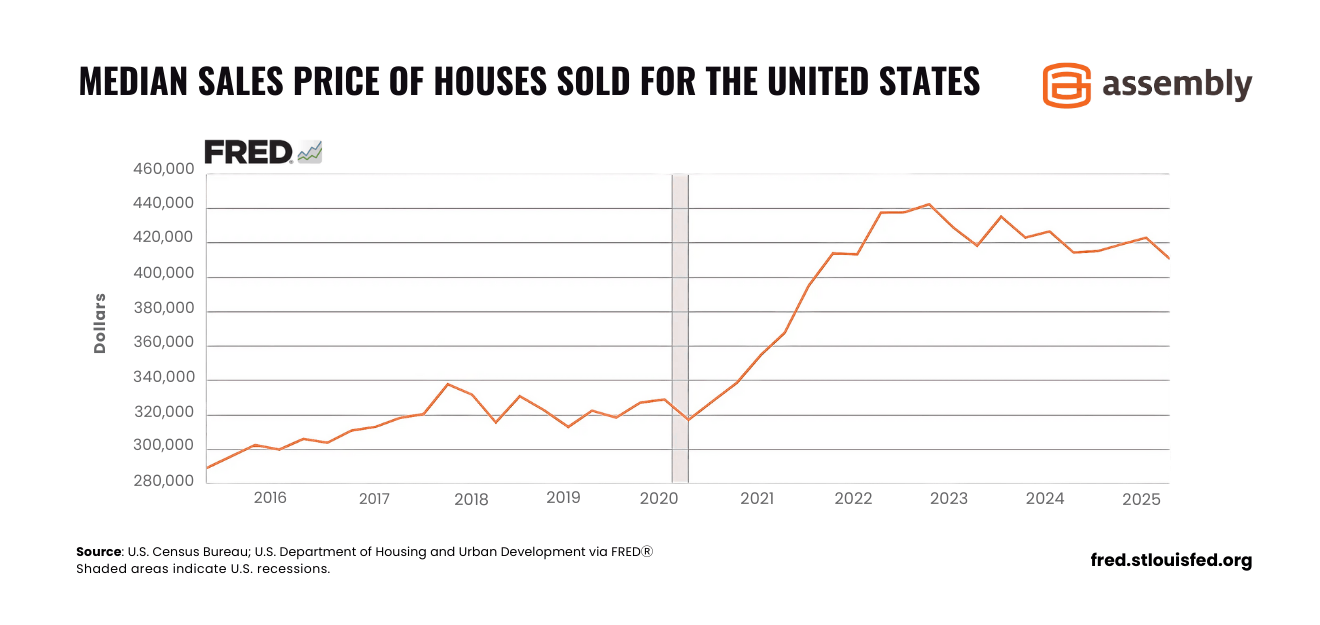

The median home price in the United States has increased about 45% in the past decade. As of this article’s publication date, the average, seasonally adjusted sale price of a single-family home or condo is: $369,147.

Click the image to view it in full size

SOURCE: St. Louis Fed

According to ATTOM, a trusted provider of real estate data, sellers made a 50% profit (on average) after selling a single-family home or condo during the first quarter of 2025. Based on the average sale price, that means the average homeseller walked away with a check for $184,573.

The words “proceeds” and “profits” are often used interchangeably, but there’s an important difference.

Proceeds = what the buyer pays

Profit = how much money remains after paying off the existing mortgage and other expenses

Other expenses may include:

If you lived in your home two out of the last five years (aggregated), some of the proceeds may be exempt from capital gains tax. The IRS doesn’t tax the first $250,000 for single filers and $500,000 for joint filers. These limits may increase in the future, but are current as of this article’s publication date.

If you don’t already have 3–6 months of living expenses set aside, now is the time. Unexpected medical bills, job loss or a change in family dynamics can wreck havoc on your finances.

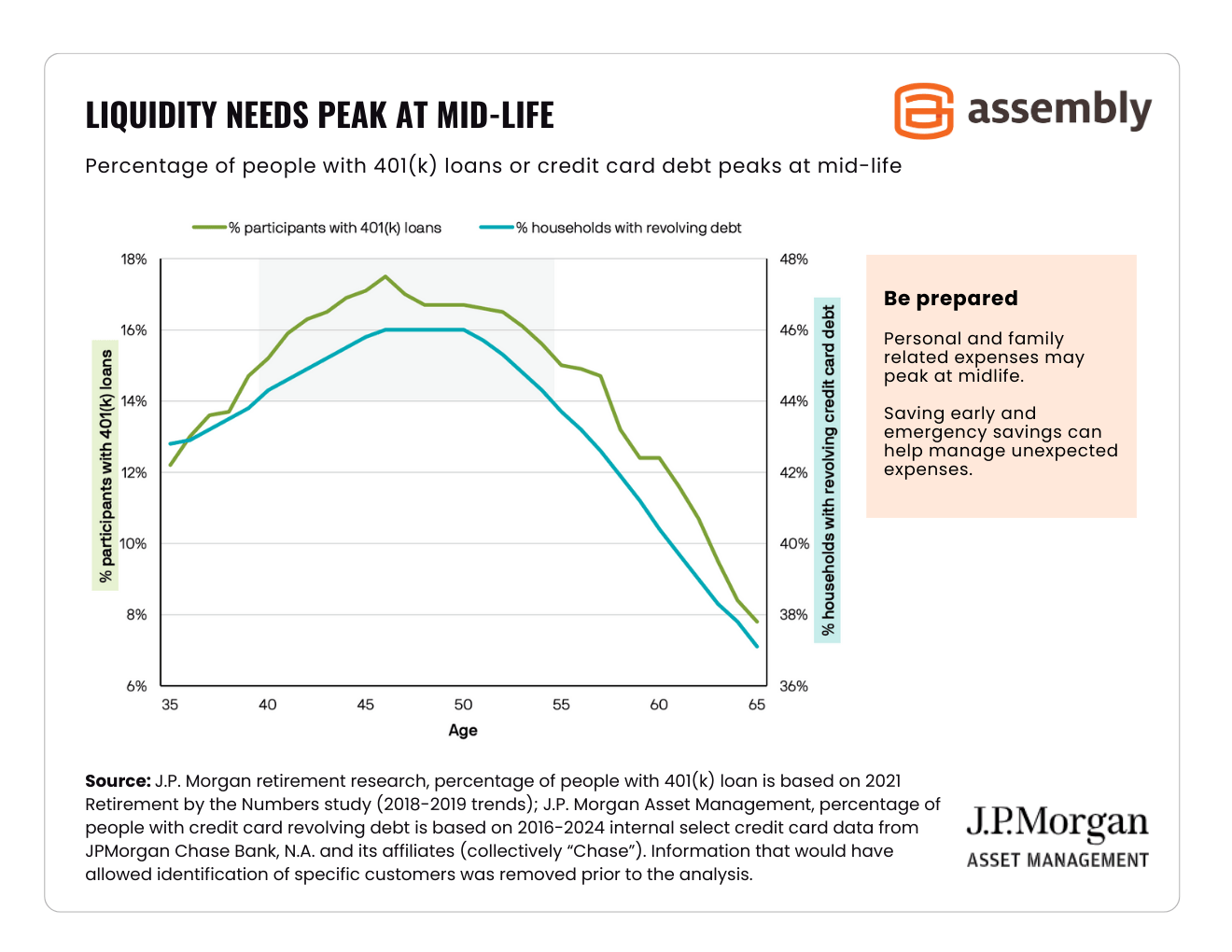

As the chart below shows, workers aged 40–55 are more likely to need liquid assets than people older than 60. But everyone should have an emergency fund, regardless of age. Emergency savings can protect you from the consequences of dipping into your retirement savings or going into debt.

Click the image to view it in full size

Source: JP Morgan Guide to Retirement 2025

Your emergency fund doesn’t have to sit in a regular savings account. Keep your money growing by investing in:

Anyone with debt, especially high-interest debt, should consider using home sale profits to pay it off. Let’s say you have credit card debt with a 20% interest rate. Paying off that debt is like earning a 20% return on your money.

Reducing debt can also improve your credit rating and reduce financial stress. It’s a win-win-win.

If you already have an emergency fund and don’t have significant debt, you could use the profits from your home sale to buy another one. A large down payment can lower your monthly mortgage payments and help you avoid private mortgage insurance (PMI).

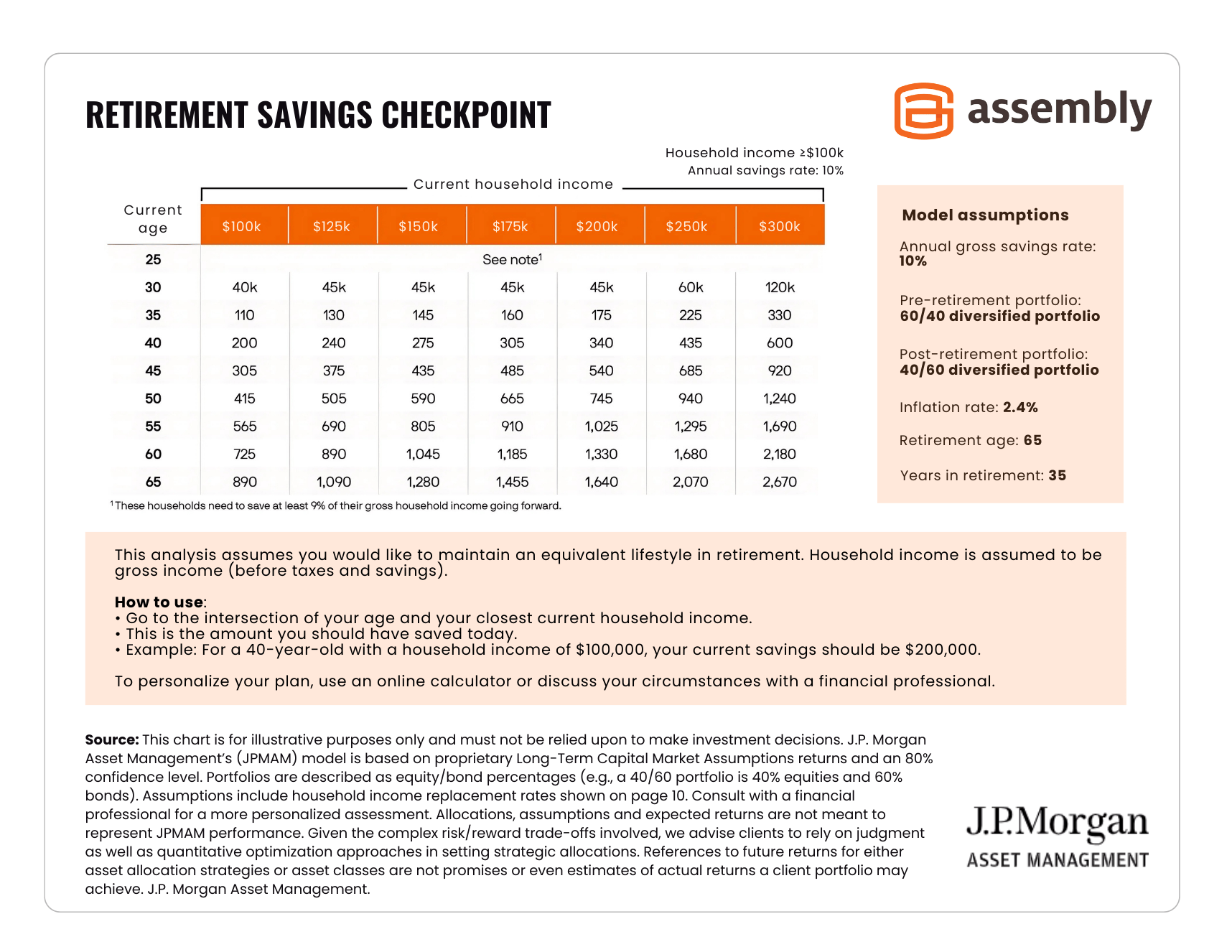

The housing market has its ebbs and flows. If it’s not a good time to buy property, it may be a good time to invest in Future You. The chart below shows benchmarks to help you evaluate your current retirement savings.

Click the image to view it in full size

Source: JP Morgan Guide to Retirement 2025

Depending on your income and eligibility, you could contribute to:

Purchasing a vacation home or rental property may be a smart move if you:

Real estate can help build long-term wealth and generate passive income. Before you buy, speak to a financial advisor about how rental income may affect your tax bill.

If you’re unsure about what to do with the profits from a home sale, a wealth manager can help you choose the best way to invest your money. We’ll start by reviewing your short-term needs and factor in your long-term dreams.

Ready to get started? Contact us online or give us a call at (415) 541-7774.

Related Reading:

Disclaimer:

Assembly Wealth (“Assembly”) is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Information presented represents an opinion as of the date published and should not be considered an investment recommendation. Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

Trump Accounts are a new type of investment vehicle to help young Americans save for the future. They have rules that are similar to an Individual...

You’ve worked hard to save and plan for a healthy financial future. Unfortunately, cybercriminals are also hard at work — devising ways to steal your...

Choosing a senior living community or retirement home can feel overwhelming, especially if you only have a short timeframe to decide. Use the...