Doug Hutchinson

Doug Hutchinson

Clear Answers to FAQs About the Budget Reconciliation Bill

The 2025 budget reconciliation bill includes a mix of new deductions, extensions to provisions from the 2017 Tax Cuts and Jobs Act and a phase-out of...

An estate plan can guide distribution of your assets after you're gone. But gifting money to family and donating to charity while you’re still alive allows you to:

Gifting money to family and donating stock to charity are two ways to leave a meaningful legacy. There are, however, rules and limits to be aware of. This article covers what you need to know, including:

A multi-year gifting strategy can help ease the financial worries of loved ones and your favorite charities. A charitable giving strategy can also reduce your tax bill and minimize taxes on your estate, but you have to make the right moves at the right time.

If you plan to give a substantial amount of money to a loved one, it may make sense to spread the gift over multiple years to avoid tax consequences. In 2025, you can gift up to $19,000 per person without having to file a tax form (this amount is adjusted for inflation each year).

Gifts that exceed the annual threshold must be reported to the IRS on a US Gift Tax Return form. It is the responsibility of the giver to file this form.

Gifting to loved ones over time removes the gifted amount from your estate, potentially easing the tax burden on your heirs after you pass away.

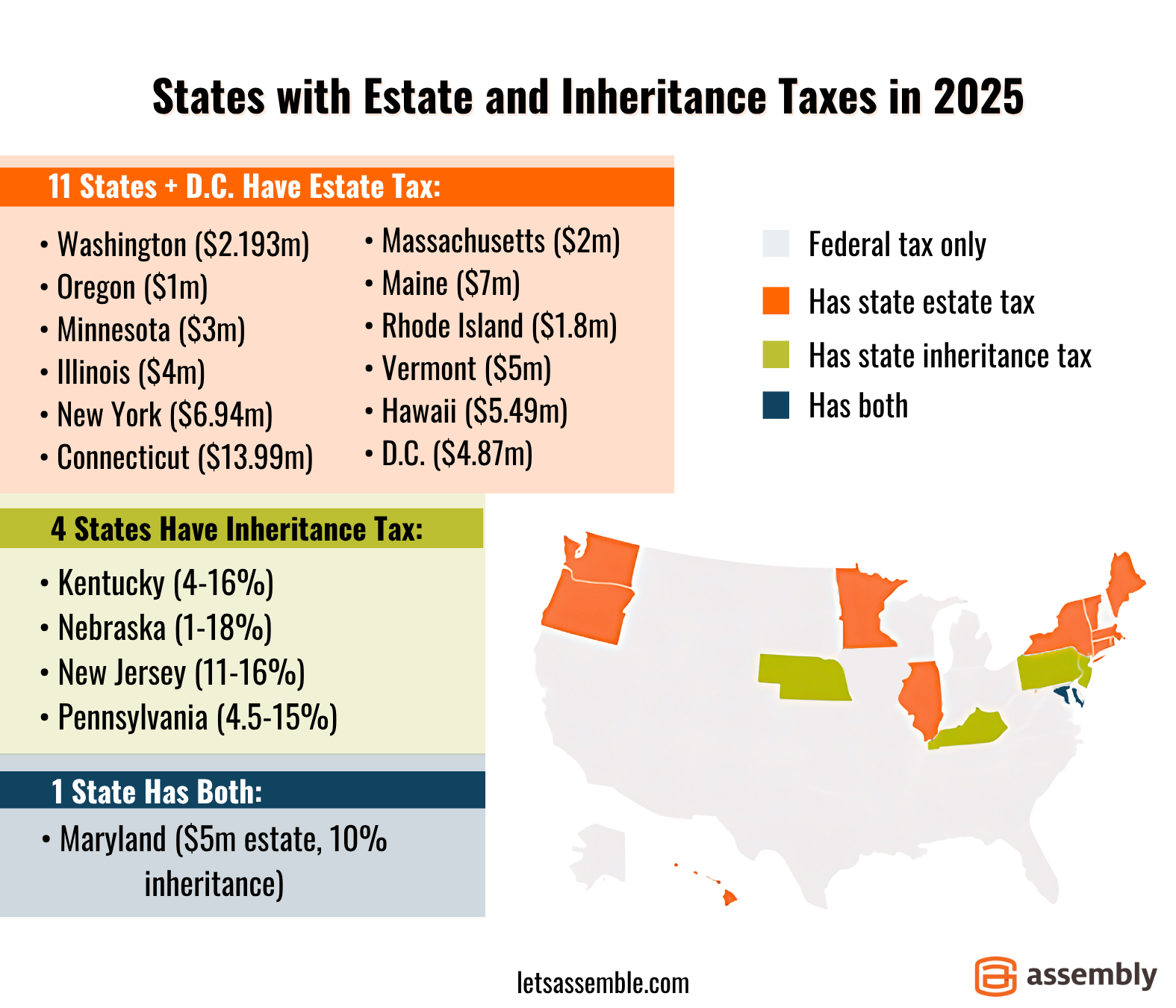

Currently, the lifetime federal gift tax and estate exemption is $13,990,000 per person. Any annual gift amount above the threshold ($19,000 in 2025) will be applied against this lifetime gift and estate exemption.

In other words, a person who passes away in 2025 will have the $13,990,000 exemption applied to the value of their estate and the sum of any annual gifts given in their lifetime above the annual gift limit each year. Estates above the exemption amount can be subject to a federal estate tax rate as high as 40%.

There are two other factors to keep in mind:

#1 The estate exemption is always subject to future changes by Congress. We don’t know what exemption threshold will be five, ten, or twenty years from now. Even if your estate is currently under the current $13,990,000 threshold, it may not necessarily be under a new, potentially lower threshold years from now.

#2 Some states have estate taxes and/or inheritance taxes. If you live in one of these states, it makes sense to work with a financial advisor who can help navigate all of these various complexities.

Click the image to view it in full size.

A Qualified Charitable Distribution (QCD) allows you to donate up to $108,000 (in 2025) from your Individual Retirement Account (IRA) directly to a qualified charity. QCDs can count toward satisfying your Required Minimum Distributions (RMDs) for the year and are not subject to income taxes.

Unlike a regular distribution from a retirement account, a QCD is not treated as taxable income. Also, lowering your IRA balance means your RMD amounts in future years will be lower. In some cases, it makes sense to start doing QCDs promptly at age 70 ½ to help lower your future tax burden in years to come.

When you open a Donor-Advised Fund (DAF) you receive an immediate tax deduction for the amount contributed to the DAF. Once established, you can direct funding to your favorite charities from the DAF over time.

DAFs are a great tool to support philanthropic causes over many years while also providing a tax benefit to the donor. As mentioned above, you can choose which organizations benefit from your fund.

If you have stock or other appreciated assets you’d like to donate to charity, here are a few strategies to consider:

Giving your stock (or other asset) directly to the charity is typically more tax efficient than selling the asset and donating the proceeds. By donating an appreciated asset, you can avoid paying capital gains tax on the increase in value. You can also deduct the fair market value of the donated asset from your income taxes in the year of the donation, up to the overall amount allowed by the IRS.

Making several years’ worth of charitable contributions in a single year (bunching) may reduce your tax burden compared to donating smaller amounts every year. This strategy typically benefits taxpayers who are close to the standard deduction threshold.

As you may know, charitable donations are only tax deductible when the taxpayer’s itemized deductions (including charitable giving) add up to more than the standard deduction.

Our friendly and experienced Wealth Managers can analyze your financial situation and help you create a gifting strategy that minimizes taxes and maximizes the amount gifted to your family and favorite charities. For example, a stock holding with substantial unrealized capital gains would typically be a better candidate for a donor-advised fund donation or a charitable contribution than a gift to a family member.

Whatever your situation, we’re here to help you build out a plan to make gifting smarter, easier, and aligned with what matters most to you. To get started, contact us online or give us a call at (415) 541-7774.

We also have a free guide that outlines how to give with greater impact and greater tax efficiency. Download our Smart Giving Playbook.

Related Reading:

Disclaimer:

Assembly Wealth (“Assembly”) is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Information presented represents an opinion as of the date published and should not be considered an investment recommendation. Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

The 2025 budget reconciliation bill includes a mix of new deductions, extensions to provisions from the 2017 Tax Cuts and Jobs Act and a phase-out of...

To ensure your assets are distributed in accordance with your wishes, detailed financial planning is essential. Without a legal will, up-to-date...

Charitable donations are an effective way to reduce your taxable income while also giving back to your community. According to a recent survey, 64...