Doug Hutchinson

Doug Hutchinson

Paying for a child’s education is an expensive undertaking, and student loan debt can make the cost even higher. Understandably, many parents want to save for their child’s education, but they might not know how and when to start.

A 529 Plan is a good option for most families because earnings and withdrawals are tax-free (at the federal level) when used to pay for qualified educational expenses. Here are a few important considerations:

College Cost Projections

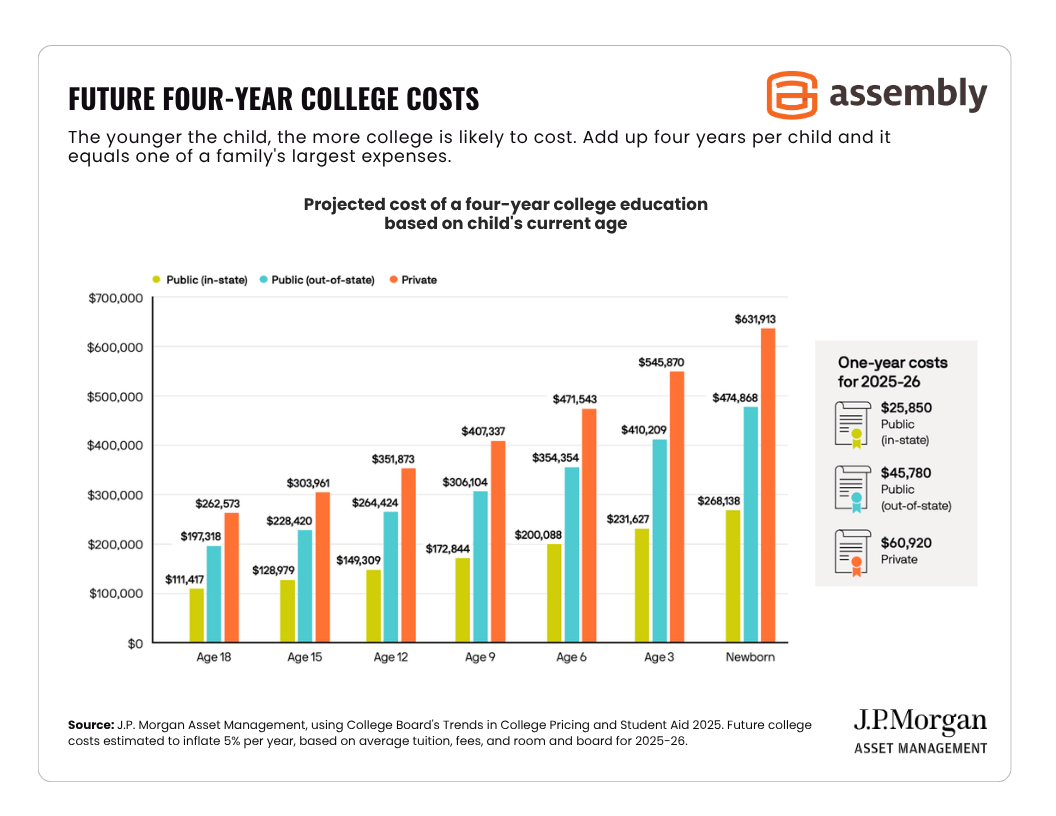

The future cost of a college degree depends on the child’s age and the type of school they choose. The chart below shows the expected cost of a four-year college education at in-state, out-of-state and private institutions (assuming costs grow by 5% per year). For a more precise estimate based on your child’s exact age and the state where you live, use this college savings plan calculator.

Click the image to view it in full size

SOURCE: J.P. Morgan College Planning Essentials

The College Board recently reported the cost of a four-year degree at a public institution is increasing (slightly) faster than inflation. To make matters worse, tuition and fees at many private colleges and universities already exceed the new federal student loan caps.

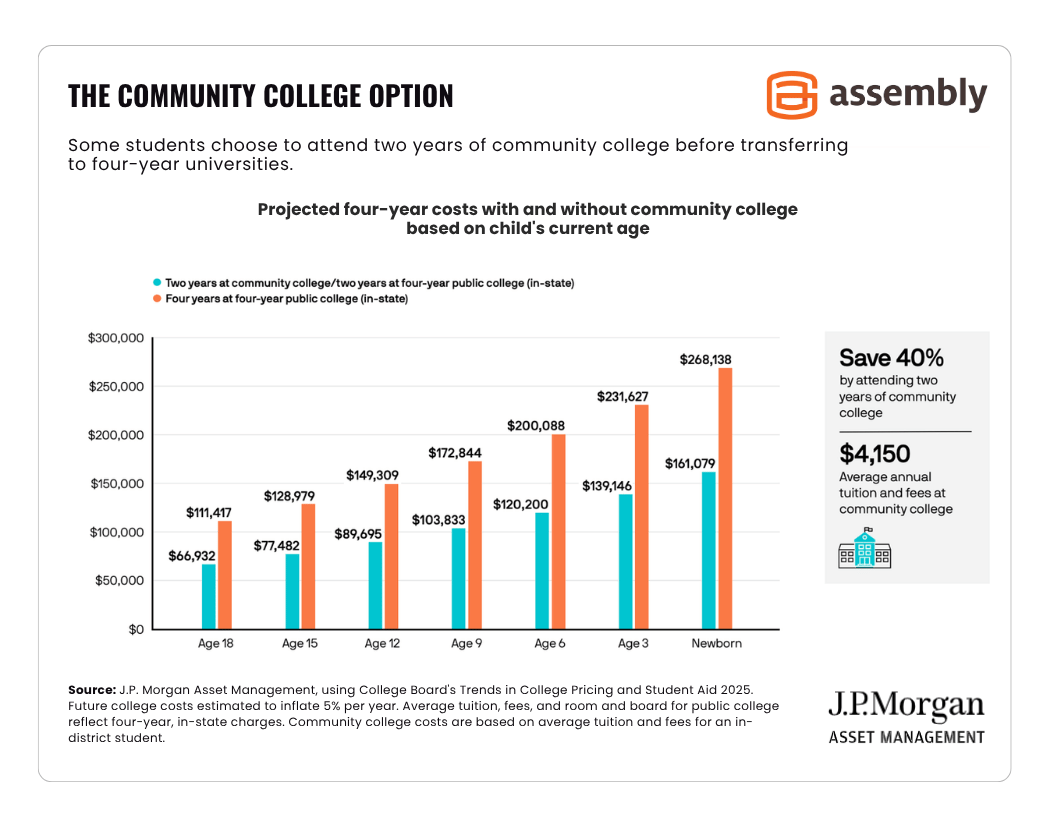

Consider Community College

Families can save up to 40% on tuition if their child attends a local community college for two years before transferring to a public, in-state college.

Click the image to view it in full size

SOURCE: J.P. Morgan College Planning Essentials

No matter which path the child chooses to take, a 529 Plan can help cover the costs.

How Does a 529 Account Work?

The first step is to open a 529 account in the state where you live. 529 Plans are typically open to residents of any state, but some states require taxpayers to use their 529 Plan to receive a state tax benefit.

In some scenarios, an out-of-state plan with lower fees may be more beneficial. A financial advisor or tax professional can guide you in the right direction.

Earnings and withdrawals on a 529 Plan are tax-free (at the federal level) when used to pay for qualified educational expenses.

What if My Child Wants to Attend a College in a Different State than the 529 Plan?

Funds from a 529 account can be used for qualified educational expenses at any eligible institution nationwide. So, for example, if you’re contributing to a 529 Plan in California, you can withdraw money to pay for a college in Arizona.

That said, there is a type of 529 Plan called a Prepaid Tuition Plan which lets you lock in today’s tuition rates at an in-state public school. These prepaid plans can usually be used at an out-of-state school, but they might not cover the full tuition cost. It depends on the plan.

If you (or your child) are unsure what school they will choose, a 529 Savings Plan typically allows for more flexibility than a 529 Prepaid Tuition Plan.

Do 529 Plans Have Contribution Limits?

Yes and no. There is no defined contribution limit at the federal level, but the IRS also states, “Contributions can not exceed the amount necessary to provide for the qualified education expenses of the beneficiary.”

The generally accepted guideline is five years of tuition, room and board at the most expensive college in the U.S. The maximum balance of a 529 account cannot exceed this amount.

To get an idea of what this cap might be, take a look back at the first chart in this article. The average cost for tuition, fees, room and board are projected to be:

- $631,913 for a child born in 2025

- $471,573 for a kindergartener

- $351,873 for a 6th-grader

The amounts listed above are the average costs. But the limit is for the most expensive school in the U.S. which, as of writing, is USC.

There are three other things families should keep in mind regarding 529 contributions:

#1 Some states have maximum contribution limits for their 529 Plans, ranging from $235,000 in Georgia to $621,411 in New Hampshire.

#2 The maximum balance is the combined total of everyone who puts money in the account (parents, grandparents, aunts and uncles, etc.)

#3 The federal gift tax may apply if a single beneficiary receives more than $19,000 in 529 contributions, cash, property, stock etc. from a single person ($38,000 for a couple) in one year.

That said, the IRS allows families to “superfund” a 529 Plan with five years’ worth of contributions in a single year ($95,000 for an individual, $190,000 for a married couple). This does not trigger federal gift taxes as long as no additional gifts are made to the beneficiary during the five-year period.

A financial advisor or tax professional can help you maximize 529 Plan contributions while avoiding any unexpected tax consequences.

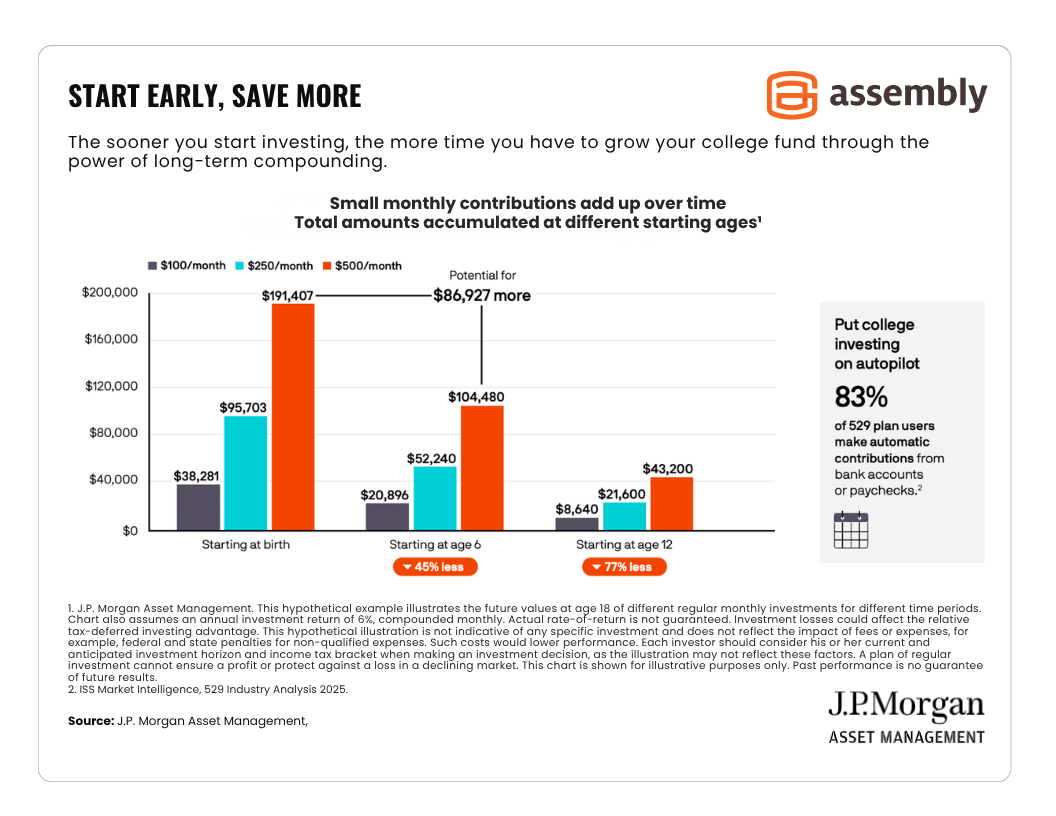

When Should I Start Saving?

Ideally, you should start saving when your child is born to maximize the benefits of compound interest. As the chart below shows, families that start saving from year one can potentially earn $86,927 more over time.

Click the image to view it in full size

SOURCE: J.P. Morgan College Planning Essentials

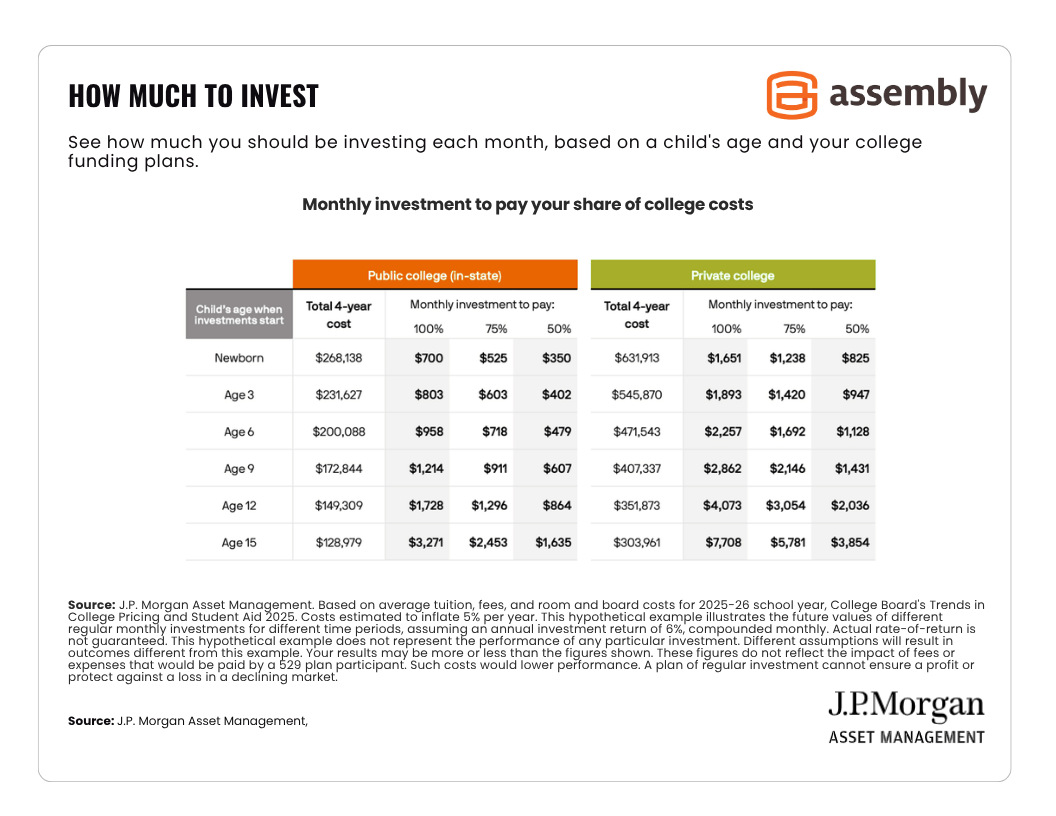

How Much Should I Invest Each Month?

The amount of money to put in a 529 each month depends on the child’s current age, how much of their education you plan to pay for and whether the student plans to attend a public or private college. The chart below reinforces the importance of investing early and also offers recommendations on how much to save if your children are older. For a more precise estimate, try this college savings calculator.

Click the image to view it in full size

SOURCE: J.P. Morgan College Planning Essentials

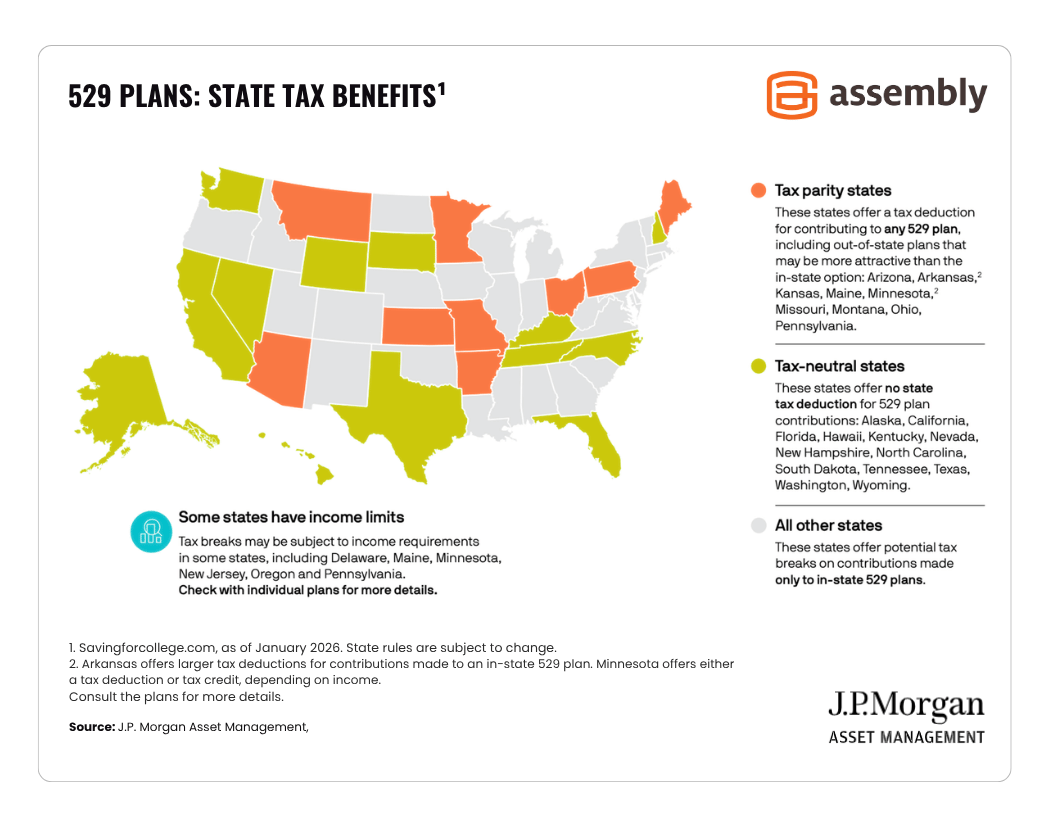

Are There State Tax Benefits for Contributing to a 529 Plan?

Some states offer a tax deduction or credit for contributions to any 529 Plan. Others only offer a tax deduction or credit for contributions made to their in-state plan.

In some states, tax benefits are only available to taxpayers under a certain income threshold. Check with your financial advisor to understand what state tax benefits you may be able to receive from contributing to a 529 Plan.

Click the image to view it in full size

SOURCE: J.P. Morgan College Planning Essentials

Should I Contribute to a Trump Account Instead of a 529?

If the goal is saving for educational expenses, a 529 Plan is typically a better option than a Trump account because a 529 Plan is a more tax efficient vehicle. Withdrawals from a 529 account to pay for qualified educational expenses are tax-free, while withdrawals from a Trump account are typically treated as taxable income.

Can I Use a 529 Plan to Pay for K-12 Education?

In 2026, up to $20,000 per student can be used from a 529 for qualified K-12 educational expenses such as tuition, books, materials and tutoring services. Please note: this only at the federal level. Some states don’t allow 529 funds to be used for K-12 expenses.

Do your homework (or consult a financial advisor) to avoid paying penalties or additional state taxes.

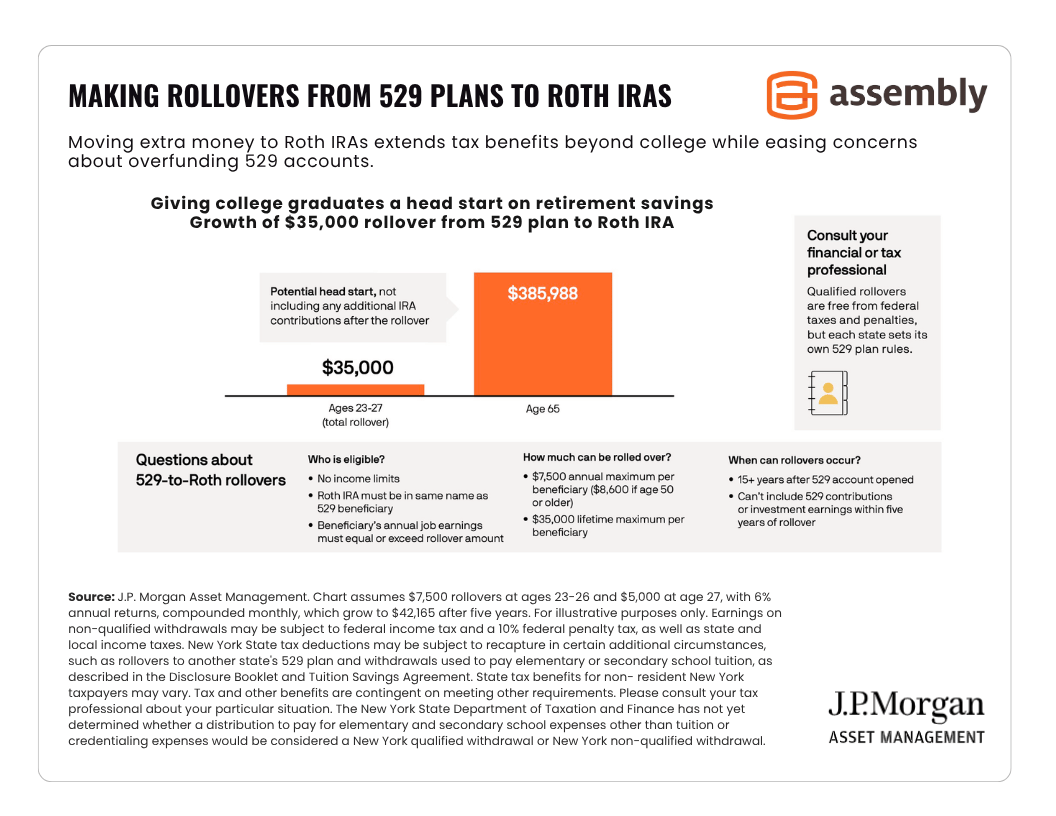

What if My Child Doesn’t Go to College?

You have a few different options if your child decides not to attend community college or a four-year institution:

- 529 funds can also be used to pay tuition and fees at trade schools and certain apprenticeship programs.

- Unused 529 funds can be transferred to a sibling without tax consequences

- 529 account holders can transfer up to $35,000 into a Roth IRA account — tax and penalty-free

Click the image to view it in full size

SOURCE: J.P. Morgan College Planning Essentials

How Do I Choose a 529 Plan?

It’s best to work with a financial advisor who can help choose a 529 Plan based on potential state tax benefits, investment options and fees. An advisor can also help weigh the pros and cons of using a Prepaid Tuition Plan versus a standard 529 Savings Plan. Most importantly, an advisor can help create a multi-year financial plan that will allow you to save for educational expenses in conjunction with other goals you may have.

A question we get asked a lot is, “How can I save for a college education and retirement at the same time without shortchanging either one?” It’s a great question and something we can help you achieve. To get started, contact us online or give us a call at (415) 541-7774.

Related Reading:

- Trump Accounts vs. 529 Plans

- Financial Planning for the Sandwich Generation

- Goal-Based Investment Planning | Build Wealth, Don't Chase the Market

DISCLAIMER: Assembly Wealth (“Assembly”) is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Certain examples contained herein are hypothetical and are provided for illustrative purposes only. These examples are based on assumed rates of return and do not reflect actual investment results. No representation is being made that any account will or is likely to achieve similar results, and actual results may vary significantly due to market conditions and other factors.

Information presented represents an opinion as of the date published and should not be considered an investment recommendation. Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.