Trump Accounts are a new type of investment vehicle to help young Americans save for the future. They have rules that are similar to an Individual Retirement Account (IRA). Parents, guardians and other authorized individuals can set up a Trump Account for any child who has not turned 18 before the end of 2026. Additionally, children born between Jan. 1, 2025, and Dec. 31, 2028 may be eligible for a $1000 contribution from the U.S Treasury.

However…even though Trump Accounts have a lot in common with IRAs, there are also special provisions and restrictions. Read on to learn more about Trump Accounts and decide if opening a Trump Account for your child or grandchild should be part of your financial plan.

We’ll cover:

Trump Accounts, also known as 530A accounts, are similar to traditional IRAs.

Trump Accounts can be opened in 2026 with the initial contributions allowed after July 4, 2026.

Trump accounts can be opened in the name of a minor (younger than 18) with a Social Security number. The child’s parents or guardians are authorized to make investment decisions on behalf of the child until the child reaches age 18.

Children born between Jan. 1, 2025 and Dec. 31, 2028 are eligible for a “jumpstart” payment of $1000 from the US government. The person opening the account must provide proof the child is a U.S. citizen with a Social Security number.

Individual Contributions

Individuals, such as a parent, grandparent, or family friend, can contribute to an account up until the child reaches 18 years old. The maximum annual contribution is $5000 total per account. The maximum contribution will be indexed to inflation starting in 2028.

Pre-Tax Employee Contributions

Pre-tax contributions are allowed for Trump Accounts if they are made through a parent’s employer’s benefit plan. Making the contributions on a pre-tax basis will allow the parent to reduce their taxable income in the year of the contribution.

Pre-Tax Employer Contributions

Employers can also contribute up to $2500 per employee to fund the Trump Account(s) of that employee’s children. If an employee has two eligible children with Trump Accounts, the maximum annual contribution would be $1250 per account.

Please note:

Money from Philanthropists

Philanthropists such as Michael Dell and Ray Dalio have announced philanthropic gifts to Trump Accounts. Dell pledged $250 for 25 million U.S. children, and Dalio will give $250 to approximately 300,000 children in Connecticut.

Funding Through States

State and local governments are permitted to contribute to Trump Accounts. As of this article’s publication date, however, state and local governments are still formalizing income eligibility rules.

Note: contributions received from governments and philanthropic organizations are not included in the $5,000 annual contribution limit.

Seed Money from the US Government

As mentioned above, the US Government will seed Trump Accounts with $1,000 for every child who is a US citizen with a Social Security number born between 2025 and 2028. There are no income limits to receive US government seed funding.

There are strict rules about what type of investments are eligible to be held in a Trump account.

On January 1st of the year the beneficiary turns 18, the account essentially turns into a traditional IRA and is subject to the rules surrounding IRA contributions and distributions. For example, the beneficiary can withdraw funds, but withdrawals before age 59 ½ are typically subject to an early withdrawal penalty.

As with other retirement accounts, there are exceptions. For example, the beneficiary can withdraw funds for educational expenses or to purchase their first home.

The beneficiary can rollover the balance of a Trump Account to an existing traditional IRA to consolidate the number of investment accounts. That said, it may make sense to do a full or partial Roth conversion to take advantage of the 18-year-old’s (presumably) low tax bracket.

Any contributions that have already been taxed cannot be taxed again, but gains and pre-tax contributions are taxable. For example:

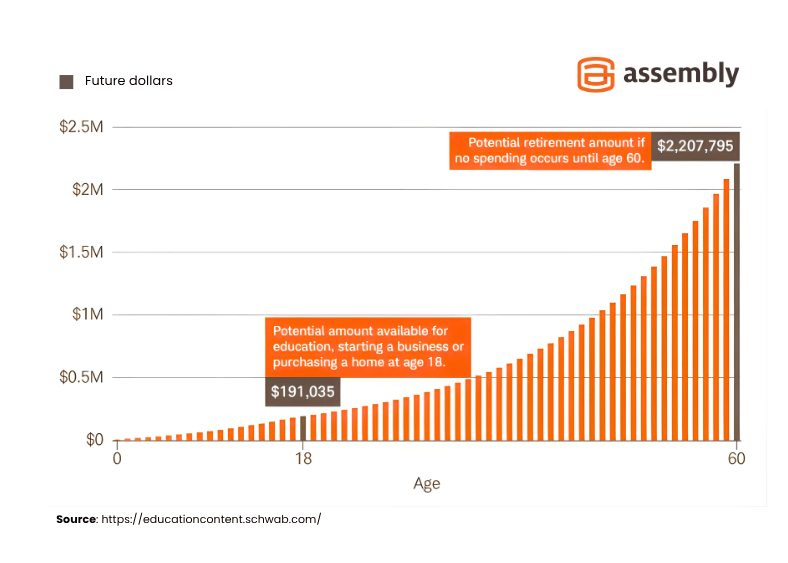

Let’s say a newborn baby named Riley has a Trump Account. Riley’s grandparents contribute $5000 from their personal savings to Riley’s account every year ($90,000 total). Thanks to the power of compound interest, the account value is $191,000 when Riley turns 18 and needs money for college.

As the example above illustrates, it’s critical to work with a financial planning expert who can analyze the pros and cons of each option and can help you reach the most optimal decision.

As mentioned above, the power of compounding can turn a $5000 annual birthday gift into $191,000 by a child’s 18th birthday. This figure is adjusted for inflation and assumes an annual return of 6% per year.

If baby Riley doesn’t make any withdrawals until age 60, the value of the account could balloon to more than $2.2 million. This calculation is made using the same 6% annual return assumption.

Click the image to view it in full size

SOURCE: Charles Schwab

While the OBBBA Act of 2025 established Trump Account tax rules at the Federal level, some states have indicated that they may impose an annual state-level income tax on Trump Account income and/or may treat employer contributions as taxable income. Since these are brand new account types, state-level legislation is evolving and will vary by state.

A tax professional can help you navigate any potential state income taxes that could be generated by Trump Accounts.

If a young adult makes a withdrawal from a Trump account, some or potentially all of the withdrawal could be subject to the “kiddie tax.” Instead of the withdrawal being taxed at the young adult’s tax rate, it would instead be subject to the parent’s (presumably higher) tax rate.

In some scenarios, a young adult making a Roth conversion may see some or all of the conversion amount be subject to the kiddie tax.

In many circumstances, it may make sense to save for a child’s educational expenses using a 529 plan rather than a Trump Account.

A Trump Account can be an attractive option due to the potential for free seed investments from governments and philanthropists, potential employer contributions and potential employee pre-tax contributions. However, parents and grandparents who want to save for a child’s educational expenses may be better off with a 529 plan given that the 529 is likely to be a more tax-efficient vehicle for funding educational expenses.

That said, Trump Accounts are an additional way to set aside money for a child’s future. They may have a place in a financial plan as part of a broad long-term savings strategy for the next generation of Americans.

Giving a child an investment vehicle with the potential for many years of compounding is a powerful gift, whether that is in the form of a Trump Account, a 529 or a UGMA/UTMA Account. To make an informed decision about which options are best for your family, connect with one of our friendly financial experts online or by phone (415) 541-7774.

DISCLAIMER: Assembly Wealth (“Assembly”) is an SEC registered investment adviser; however, this does not imply any level of skill or training and no inference of such should be made. The opinions expressed herein are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. We provide historical content for transparency purposes only. All opinions are subject to change without notice and due to changes in the market or economic conditions may not necessarily come to pass. Mention of a security should not be considered a recommendation or solicitation to purchase or sell the security, and any securities mentioned may be held by Assembly for client portfolios.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Certain examples contained herein are hypothetical and are provided for illustrative purposes only. These examples are based on assumed rates of return and do not reflect actual investment results. No representation is being made that any account will or is likely to achieve similar results, and actual results may vary significantly due to market conditions and other factors.

Information presented represents an opinion as of the date published and should not be considered an investment recommendation. Assembly does not become a fiduciary to any listener, reader or other person or entity by the person’s use of or access to the material. The reader assumes the responsibility of evaluating the merits and risks associated with the use of any information or other content and for any decisions based on such content.

{kind=link}